The 2026 Memory Crunch: Should Procurement Teams Buy Now, or Wait?

Conventional DRAM contract prices rose ninety-two percent quarter-on-quarter in the first quarter of 2026, and TrendForce has forecast a further sixty percent in Q2. NAND flash has risen fifty-seven percent and is expected to move a further seventy-to-seventy-five percent. High-Bandwidth Memory — the specialist chip on top of every AI accelerator — is, in SK hynix’s own words, “effectively sold out” through the end of 2026.

This is the steepest memory price move in more than fifteen years. It is not a conventional cycle. Procurement leaders should not treat it as one.

Three forces are driving the shock

The first is AI-infrastructure capital expenditure. The five major hyperscalers — Amazon, Alphabet, Meta, Microsoft, and Oracle — have together committed approximately six hundred and sixty billion US dollars in 2026 capex, about seventy-five percent of which is AI-related. Every AI server they buy is an upstream demand signal for HBM, server DRAM, and enterprise NAND.

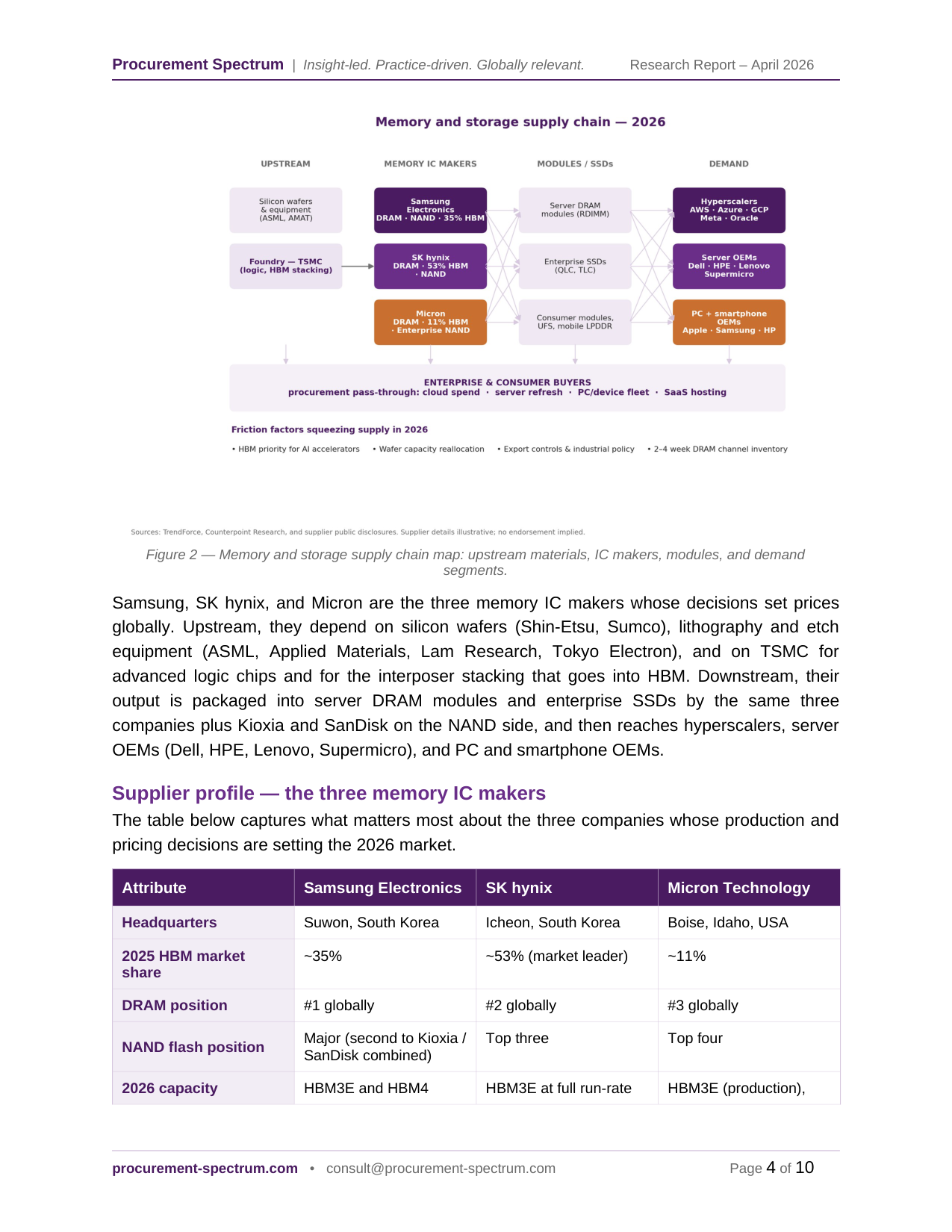

The second is a three-supplier market. Samsung, SK hynix, and Micron produce virtually all production-grade DRAM and HBM. They have each reallocated wafer capacity toward HBM and server-grade memory, which mechanically reduces the supply of conventional DRAM and NAND to everyone else. Goldman Sachs describes the resulting imbalance as the worst DRAM undersupply in fifteen-plus years.

The third is channel inventory: two to four weeks of DRAM is now held by distributors, versus eight to twelve weeks in a normal market. There is no buffer to absorb further demand shocks.

The cost is cascading to enterprises fast

The move has already reached the rest of the economy. Gartner reported finished-PC price rises of seventeen percent and smartphone rises of thirteen percent in February 2026. AWS raised its EC2 Capacity Block ML (on-demand GPU-server) rate fifteen percent in January. Server OEMs are passing cost through on every new order.

Organisations with 2026 refresh cycles for servers, storage, PCs, or smartphones are directly exposed. Organisations running memory-intensive cloud workloads are exposed through their cloud bill. Organisations whose SaaS vendors run on the same infrastructure will see the pass-through in renewal terms.

Buy now, or wait?

The evidence supports buying now for most categories. The three facts that matter are these. Contract prices are forecast to continue rising in Q2 2026, not fall. Hyperscaler capex is locked in — there is no demand reversal coming. Supply-side relief — new fab capacity from Samsung, SK hynix, and Micron — is late-2027 and 2028 business, not 2026. Waiting does not save money. It costs money and delays delivery.

What to do — tiered by category

For server DRAM, enterprise SSDs, standard PCs, and standard smartphones due for refresh in 2026: accelerate the purchase into H1 2026, negotiate fixed-price contracts with staged delivery, and consider pulling forward ten to fifteen percent of planned 2027 volumes where policy permits.

For AI-class GPU servers: the constraint is allocation, not price. Place firm orders now, pre-commit to volumes, and accept the twenty-six-to-forty-week lead times. Price negotiation on these items matters far less than queue position.

For memory-intensive cloud workloads: shift from spot and on-demand to reserved and committed-use pricing. Twelve-to-twenty-four-month commitments protect predictable consumption from further increases.

For discretionary consumer-grade spend and product-embedded memory: stage the purchase, use indexed contracts that share the price risk with the supplier, and build 2027 renegotiation windows into any multi-year agreement.

Guidance for practitioners

In a concentrated supplier market, procurement leverage does not come from competitive-tender dynamics. Four levers matter more than unit-price negotiation: multi-year volume commitment in exchange for priority allocation; supplier diversification at the module and system level; payment-term flexibility; and protective contract language on force-majeure and delivery escalation. The teams that will protect both budget and operational delivery in 2026 are the ones that treat this as an allocation-and-contract-engineering problem, not a pricing negotiation.

Subscribe to our newsletter for regular insights.